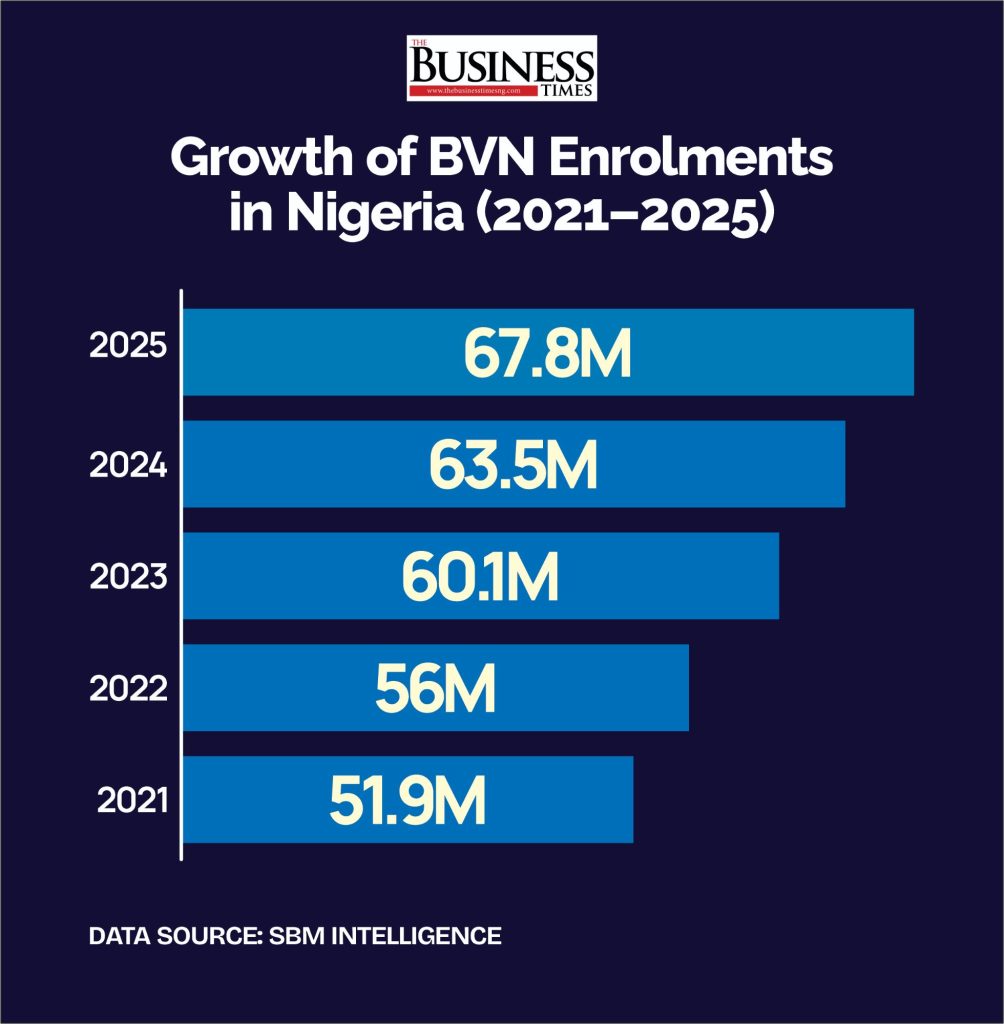

Nigeria’s Bank Verification Number (BVN) enrollment reached 67.8 million in 2025, marking another significant expansion of the country’s financial identity infrastructure. On the surface, the figure suggests progress, broader coverage, tighter regulation, and a financial system that is steadily drawing more Nigerians into its formal net. However, beneath the numbers lies a more complex economic reality. The growth of BVN enrollments, while administratively impressive, does not automatically equate to meaningful financial inclusion or measurable economic impact.

The BVN was introduced to unify customer identities across the banking system, curb fraud, strengthen know-your-customer (KYC) compliance, and support anti-money laundering efforts. Over time, it has evolved into a compulsory gateway for accessing bank accounts, digital payment platforms, and several government-linked financial services. This shift has undeniably driven enrollment growth, but it has also altered the nature of participation, raising questions about whether inclusion is being achieved by empowerment or enforcement.

Regulatory Push, Not Organic Adoption

The recent surge in BVN numbers has been largely policy-driven. Regulatory directives tying BVN compliance to account operation, mobile money access, and transaction limits have compelled millions of Nigerians to enrol. While this approach has proven effective in boosting registration figures, it blurs the line between genuine financial inclusion and forced compliance.

From an economic standpoint, inclusion is not defined by identity registration alone. A BVN-linked account that remains inactive, underfunded, or unused contributes little to savings mobilisation, credit expansion, or investment growth. This reality explains why rising enrollment figures have not translated into a proportionate expansion in retail credit, SME financing, or household financial resilience.

Public sentiment reflects this disconnect. In a poll by Business Times, assessing the economic relevance of BVN expansion, respondents were asked whether increasing BVN enrollments would boost Nigeria’s economy. The dominant response was “No, it’s just numbers on paper,” outweighing those who believed broader registration would automatically translate into growth. This view underscores a growing skepticism: Nigerians are registering, but many are not experiencing tangible economic benefits.

Inclusion Without Impact

The assumption that financial identity automatically leads to financial empowerment remains one of the weakest links in Nigeria’s inclusion narrative. BVN enrollment provides access, but access alone does not resolve structural constraints such as low income, informal employment, high borrowing costs, and limited credit availability.

For many BVN holders, registration has not resulted in easier access to loans, better insurance coverage, or lower transaction costs. Small businesses, particularly in the informal sector, continue to face strict collateral requirements and high interest rates, despite being formally identified within the banking system. As a result, BVN expansion has improved visibility without significantly improving opportunity.

This gap between policy intent and lived experience is why enrollment figures, no matter how large, cannot be treated as conclusive evidence of inclusion success.

Trust, Data, and System Credibility

Financial identity systems depend heavily on public trust. Without confidence in data protection and system integrity, compliance becomes fragile and transactional rather than cooperative. To gauge this sentiment, a poll asked Nigerians whether they trust the BVN system with their personal data.

The leading response, “Yes, my information is safe”, suggests a moderate level of confidence in the system. However, the presence of respondents who expressed concerns about privacy risks highlights an unresolved vulnerability. In an environment where data breaches and institutional accountability remain weak, trust can erode quickly. Any major compromise of BVN data would not only damage the system’s credibility but also undermine years of regulatory effort.

For policymakers, this means that expanding enrollment without simultaneously strengthening data protection frameworks is a strategic risk.

Opportunities Acknowledged, Outcomes Delayed

Despite widespread skepticism, Nigerians have not dismissed the BVN system outright. When asked whether the BVN creates new opportunities, the most selected response was “Yes, it opens opportunities.” This indicates that the public recognises the potential value of financial identity as an enabling tool.

However, potential alone does not drive economic growth. The failure lies not in the concept of BVN, but in the limited conversion of BVN-linked data into actionable economic outcomes. Credit scoring models remain underdeveloped, BVN-backed lending is still limited, and integration with tax, social welfare, and enterprise support systems remains weak.

In effect, Nigeria has built a wide front door into the financial system, but too few productive pathways inside it.

The Cost of a Numbers-First Narrative

One of the most significant policy risks is the tendency to treat BVN enrollment growth as an end in itself. This numbers-first narrative diverts attention from more meaningful indicators such as account activity, credit penetration, SME loan performance, and household financial stability.

Economically, the opportunity cost is substantial. BVN data could be leveraged to reduce information asymmetry in lending, lower default risks, and expand credit to underserved sectors. When this does not happen, the system’s value is underutilised, and public confidence weakens.

The poll responses reinforce this reality: Nigerians are willing to engage with the system, but they are increasingly demanding outcomes rather than metrics.

Structural Barriers Remain Intact

BVN expansion operates within a broader financial environment still constrained by informality, poverty, and weak institutional coordination. Rural populations and informal workers often register BVNs but remain excluded from meaningful financial services due to poor infrastructure, low digital literacy, and high transaction costs.

Without targeted interventions to address these barriers, BVN enrolment risks becoming a symbolic exercise, broad in coverage but shallow in impact.

From Compliance Tool to Economic Infrastructure

For BVN to evolve into a true economic enabler, policy focus must shift decisively from enforcement to utilisation. This requires:

Linking BVN data to affordable credit for SMEs and micro-entrepreneurs

Strengthening consumer data protection and accountability mechanisms

Using BVN analytics to improve social welfare targeting and tax efficiency

Measuring success through economic participation, not registration volume

Only through this transition can BVN justify its growing centrality in Nigeria’s financial architecture.

Conclusion: Progress With Conditions

Reaching 67.8 million BVN enrollments is a notable administrative achievement. It reflects regulatory determination and increasing digital penetration across the financial system. However, the economic value of this progress remains conditional.

As public opinion makes clear, Nigerians are no longer impressed by scale alone. Until BVN enrolment translates into broader access to credit, lower financial exclusion, and measurable improvements in economic wellbeing, it will remain, accurately described by many as numbers on paper.

The infrastructure now exists. What remains is the harder task: converting financial identity into real economic value.