On January 16, 2026, Nigeria’s Securities and Exchange Commission (SEC) issued a circular revising minimum capital requirements for nearly all capital market operators. The 2015 framework is replaced with a forward-looking regime designed to enhance market resilience, protect investors, and regulate previously under-supervised digital finance actors. The implications affect market structure, competition, innovation, and systemic stability.

The reforms increase financial buffers for brokers, dealers, fund managers, fintech operators, and market infrastructure providers. Effective June 30, 2027, the new requirements signal a shift from permissive oversight to prioritizing risk absorption and operational strength. Oyetunde Gabriel, financial adviser, notes, “The SEC raised capital requirements to address liquidity gaps, high leverage, and potential default risks. Strengthening capital buffers ensures firms can absorb losses, meet obligations, and maintain orderly trading.”

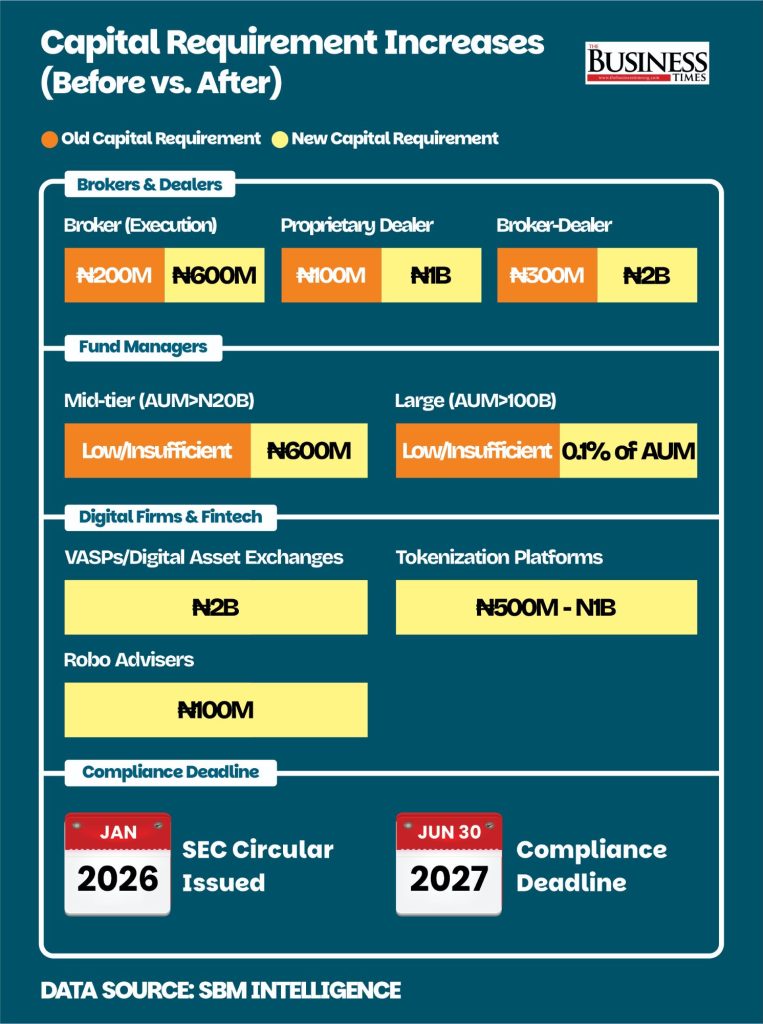

Capital Requirements Across Participants

Securities brokers offering client execution services must hold ₦600 million, up from ₦200 million. Proprietary dealers trading on their own account must maintain ₦1 billion, a tenfold increase from ₦100 million. Integrated broker-dealers now require ₦2 billion, compared with ₦300 million previously. “Higher capital cushions reduce the probability that an intermediary’s failure transmits distress throughout the financial system,” Gabriel explains.

Fund and portfolio managers face tiered capital floors aligned with assets under management (AUM). Managers with over ₦20 billion in assets must hold ₦5 billion. Mid-tier managers must maintain ₦2 billion. Large managers above ₦100 billion AUM are required to hold 0.1 per cent of assets. Gabriel clarifies, “New capital thresholds were set using stress tests, historical market data, and risk models simulating extreme conditions to ensure solvency while remaining achievable for different types of market participants.”

Digital finance operators now face explicit obligations. Virtual Asset Service Providers, including exchanges and custodians, must hold ₦2 billion. Tokenisation platforms maintain ₦500 million to ₦1 billion. Robo-advisers must hold ₦100 million. “The regulation signals formalization, establishing standards and investor protections for digital asset and fintech firms,” Gabriel says. “Compliance enhances credibility, reduces operational risk, and creates a safer environment for sustainable growth.”

Issuing houses, registrars, trustees, and underwriters also see capital increases. Full-service underwriting houses must hold ₦7 billion, advisory-only houses ₦2 billion, registrars ₦2.5 billion, trustees ₦2 billion, and composite exchanges or central counterparties ₦10 billion. Gabriel emphasizes, “Adequate capital reduces the risk that the failure of one intermediary threatens the broader market, safeguarding clients and counterparties.”

Policy Objectives

The SEC’s revisions aim to strengthen market resilience, protect investors, integrate innovation, and align Nigeria with global standards. “Higher capital buffers enable firms to absorb shocks without destabilizing clients or requiring government support,” Gabriel observes. “Investor protection improves as firms can honor obligations under stress, reinforcing confidence in market integrity.” Digital finance integration creates a regulated perimeter for innovation, ensuring that risk and capital align with international best practices.

Market Implications

Smaller brokers, fund managers, and fintech firms may struggle to meet thresholds, prompting fundraising, mergers, or exits. Gabriel notes, “Smaller brokers, fund managers, and fintech firms may face challenges meeting the new capital thresholds. While compliance creates short-term pressures, it strengthens resilience, reduces default risk, and protects investors over the long term.”

Consolidation is likely. While competition may decline, stronger, well-capitalized firms can absorb shocks and maintain operations. Digital firms face a choice: scale to meet capital requirements or focus on niche operations. “Capital adequacy is now a precondition for legitimacy, not an optional nicety,” Gabriel states.

Key metrics will reveal the reforms’ effectiveness. Capital adequacy, liquidity ratios, leverage, trading continuity, volatility, and investor sentiment indicate whether stability improves. Gabriel adds, “Investors and analysts should track capital adequacy, liquidity ratios, leverage, and default incidents. Market indicators such as volatility, bid-ask spreads, trading continuity, and investor sentiment reveal whether firms can withstand shocks while maintaining efficient operations.”

The SEC has redefined market expectations. Brokers, fund managers, digital firms, and infrastructure providers face new capital standards. Compliance will require restructuring, fundraising, and potential consolidation. Long-term benefits include stronger market stability, enhanced investor confidence, and an environment where innovation competes on governance and financial strength. Gabriel concludes, “The capital market landscape in Nigeria is entering a new era, one defined by robustness, discipline, and structural soundness. Strategic adjustments must begin immediately, even as compliance deadlines extend into 2027.”