In the third quarter of 2025, Nigeria’s economic data delivered a headline figure that sparked cautious optimism: a balance of payments surplus of $4.60 billion. Reported by the Central Bank of Nigeria (CBN), this figure marks a stark reversal from the deficit position of the previous quarter and, on the surface, suggests a significant strengthening of the nation’s external position amidst a long history of foreign exchange shortages, reserve depletion, and capital flight.

A surplus in the balance of payments—the ledger that tracks all economic transactions between a country and the rest of the world—occurs when total inflows of foreign exchange exceed outflows. For Nigeria, such a moment is undeniably significant, offering a reprieve from external pressures and hinting at improved FX dynamics. However, a deeper, more nuanced analysis reveals a harder truth. This surplus, while real and economically meaningful in the short term, is less a sign of completed structural transformation and more a reflection of acute adjustment pressures and cyclical gains.

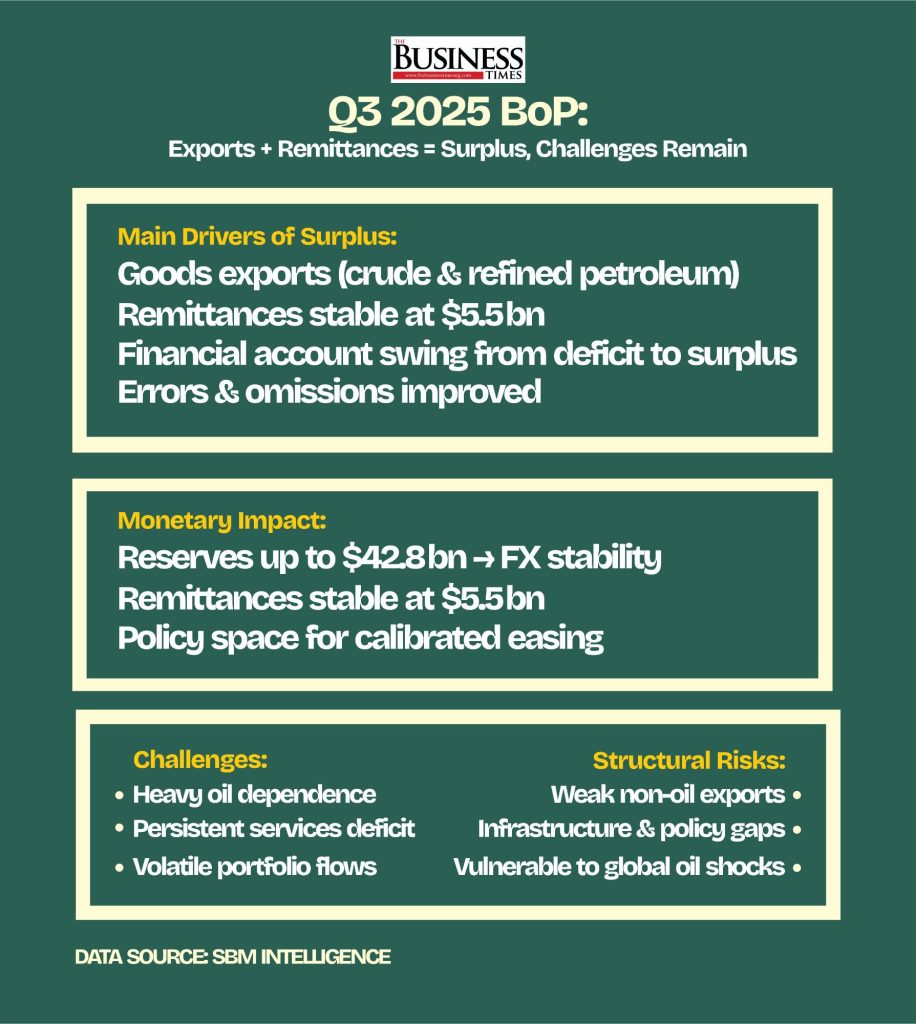

It is a snapshot of an economy in the midst of recalibration, one that remains profoundly exposed to volatility and concentrated risks, where progress is tangible but permanence is far from assured.To understand the composition and fragility of this surplus, one must dissect its three primary drivers, as detailed in the Q3 2025 data. The first and largest contributor was a substantial goods trade surplus, which reached $4.94 billion. This was supported by total export earnings of $15.24 billion. Within this, a critical and notable shift was observed. Crude oil exports, the traditional mainstay, rose to $8.45 billion. More importantly, refined petroleum exports surged to $2.29 billion, representing a sharp quarterly increase.

This development is economically meaningful because it signals a partial correction of a decades-old structural imbalance. Historically, Nigeria has exported crude oil only to spend a significant portion of its earnings re-importing refined petrol, diesel, and other products, a practice that chronically strained foreign exchange reserves. The Q3 data showed a 12.7 percent decline in refined fuel imports, directly linked to the growing output from the country’s revitalized domestic refining capacity. The export of refined products, therefore, is not just a new line item; it represents a move toward capturing more value within the country and reducing a persistent drain on FX.

Yet, these gains are immediately tempered by their narrow concentration. As analyst Adetayo Bolanle notes, “The surplus looks fragile. It was largely supported by improved oil receipts, refined petroleum exports, and short-term capital inflows reacting to FX reforms.” Crude oil and petroleum products together continue to dominate Nigeria’s export profile, meaning the nation’s external health remains inextricably tied to global oil prices, the stability of its own production (often hampered by outages and theft), and worldwide energy demand dynamics. Non-oil exports, despite policy rhetoric, remain marginal in both scale and impact. The sustainability of the refined fuel export boom itself is not guaranteed. As Bolanle further observes, “Refined petroleum exports played a meaningful role, helping reduce fuel import costs and generating new FX inflows, especially with local refining capacity expanding. However, sustainability depends on stable crude supply, competitive pricing, and efficient refinery operations.” Any disruption—from feedstock supply issues to operational hiccups or shifts in international refining margins—could quickly weaken this nascent but vital contribution.

The second pillar of the Q3 surplus was the secondary income account, which recorded a $5.50 billion surplus. This was overwhelmingly powered by diaspora remittances, which totaled $5.24 billion. These inflows represent one of Nigeria’s most reliable and resilient sources of foreign exchange, acting as a critical stabilizing buffer for the entire economy. Remittances provide direct support to household consumption, alleviate poverty, and, crucially, bolster FX liquidity without adding to debt. They reduce the constant pressure on the CBN’s official reserves by supplying dollars directly into the system, often through informal or parallel channels that complement official windows.

However, to classify strong remittances as a policy success or a structural economic gain would be a misreading. Remittance flows are essentially exogenous; they are determined by the health of external labour markets, the income levels of the Nigerian diaspora, and global economic conditions. As Bolanle emphasizes, “Remittance flows depend on external labour markets and diaspora income conditions, not domestic productivity.” While invaluable for stability and welfare, remittances do not stimulate productive capacity within Nigeria. They are not a lever that policymakers can directly pull to generate growth, nor do they substitute for the hard work of building export-led industries or enhancing structural competitiveness. They provide a cushion, but not an engine.

The third factor behind the improved BoP position was a temporary amelioration in the financial account, which moved to a net lending position of $0.32 billion. This reversed the large net borrowing seen in the second quarter and was supported by a combination of foreign direct investment (FDI), which amounted to $0.72 billion, and portfolio inflows, which were a more substantial $2.51 billion. This shift indicates a period of more willing engagement by foreign investors during Q3, likely reacting to a confluence of factors: adjustments in the exchange rate that presented a more realistic valuation, consequent higher yields on naira-denominated assets, and perhaps improved transparency in the FX market following recent reforms.

This improvement, however, is inherently tactical rather than structural. Portfolio investment—the “hot money” that flows into stocks and bonds—is notoriously volatile and reversible. It is highly sensitive to global interest rate trends (particularly decisions by the U.S. Federal Reserve), shifts in global risk sentiment, and perceptions of domestic policy credibility. The $2.51 billion inflow could easily reverse in the next quarter if investor sentiment sours. Meanwhile, the FDI inflow, while a positive sign, remains modest relative to the size and needs of Africa’s largest economy. It points to a continued confidence deficit among long-term, bricks-and-mortar investors. As highlighted by Tobi Johnson, “Nigeria needs policy consistency, credible FX management, and a clearer legal framework for investors.”

To convert tactical interest into structural commitment, Nigeria must deepen reforms that address foundational concerns: unreliable infrastructure, weak contract enforcement, regulatory uncertainties, and security challenges. Targeted incentives can help, but only if embedded within a coherent and predictable policy environment that convinces investors to commit capital for the long haul.One of the most tangible and consequential outcomes of the Q3 surplus was its direct impact on Nigeria’s external reserves. The reserves rose from $37.81 billion to $42.77 billion, crossing a psychologically important threshold. This accumulation strengthens Nigeria’s ability to meet external debt obligations, smooth out import payments, and, critically, boosts confidence in the FX market. Higher reserves provide the monetary authorities with more breathing space and reduce the need for aggressive, distortionary interventions to defend the naira. They are a vital buffer. Yet, as with the surplus itself, reserves are a tool for management, not a solution to underlying imbalances. Tobi Johnson notes, “Higher reserves can help smooth FX volatility and boost confidence, which may support the naira. However, reserves alone won’t curb inflation.” Reserves can be depleted as quickly as they are built if the fundamental drivers of FX demand—such as import dependency—are not addressed.

This leads directly to the implications of the BoP surplus for the Nigerian naira and the country’s debilitating inflation. A balance of payments surplus does not automatically guarantee currency stability, but sustained surpluses do improve the conditions for it. For Nigeria, the Q3 developments create a more favorable environment: improved FX inflows from exports and remittances reduce acute scarcity, higher reserves enhance the CBN’s firepower and market confidence, and reduced demand for FX to pay for fuel imports directly lowers a major source of pressure. If these trends continue, they could indeed help moderate the wild volatility that has characterized the naira in recent years.

However, the domestic battle against inflation is fought on a different, though related, front. Inflationary pressures in Nigeria are deeply structural, rooted in monetized fiscal deficits, pervasive supply-chain disruptions, agricultural insecurity, and high logistics costs. The BoP surplus may create valuable policy space by easing external constraints, but it does not directly solve these domestic issues. The circulation of naira liquidity within the economy, driven by government spending and CBN financing, continues to fuel demand-pull inflation. Therefore, while the external sector shows signs of adjustment, the internal economy remains under severe strain. The surplus offers an opportunity, not a guarantee; it provides policymakers with a moment to implement complementary fiscal and monetary tightening and supply-side reforms without the immediate panic of a collapsing currency.

Ultimately, the hard truth illuminated by the Q3 2025 data is that this surplus demonstrates adjustment, not transformation. The positive signals are clear and should be acknowledged: reduced refined fuel import dependence, higher overall export earnings, improved reserve buffers, and better FX accounting transparency are all steps in the right direction. They are the results of difficult adjustments, including currency reforms and the painful but necessary reduction of costly petrol subsidies.Yet, the unresolved constraints that have plagued Nigeria for decades persist unabated. The risk of export concentration is as acute as ever. Weak non-oil competitiveness means the country struggles to sell manufactured or agro-processed goods on the global stage. The services account continues to run a deficit, as Nigerians spend more on foreign travel, education, and professional services than the country earns. Investor confidence, while improved in the quarter, remains fragile, contingent on the next policy move or political development. Without sustained diversification, genuine industrial growth, and broad-based productivity gains, the balance of payments could easily swing back into deficit under less favorable global conditions. As Adetayo Bolanle succinctly warns, “Nigeria remains highly exposed. Oil still accounts for most export earnings and FX inflows, so a price drop or output shock would directly pressure the balance of payments, reserves, and the naira.”

In conclusion, the $4.60 billion balance of payments surplus for Q3 2025 is a confirmation that Nigeria’s external sector is stabilizing after a period of prolonged and intense stress. It is a necessary and welcome step forward. However, it is decidedly not a finish line nor a victory lap. For this moment of adjustment to crystallize into a lasting structural shift, Nigeria must embark on the more arduous path of scaling non-oil exports, deepening domestic value addition across all sectors, converting temporary FX stability into sustained real sector growth and job creation, and anchoring investor confidence through unwavering policy consistency. The quarter shows measurable progress, but whether it will be remembered as a genuine turning point in Nigeria’s economic history depends entirely on what comes next. The window of opportunity provided by this surplus is open, but it will not remain so indefinitely. The task of transformation—moving from cyclical adjustment to foundational resilience—remains the defining challenge.